The Capital Markets Authority (CMA) has licensed three new corporate trustees to support the growin…

In February 2025, the Capital Markets Authority (CMA) has licensed Tradiam Investments Services Lim…

The Capital Markets (Collective investment schemes) Regulations 2023, gazetted on 15th December, 20…

The Capital Markets (Alternative Investment Funds) Regulations 2023, was gazetted on 15th December,…

The Capital Markets (Alternative Investment Funds) Regulations, 2023, was issued in October 2023 by…

The Capital Markets (Collective Investment Schemes) Regulations, 2023, was issued in October 2023 b…

The guidance to Fund Managers of Collective Investment Schemes (CISs) on Valuation, Performance Mea…

On 12th June 2020, the Capital markets Authority (CMA) Issued an Circular on the requirements for c…

The first-ever student’s unit trust fund in Kenya was launched in under the name Wanafunzi Investme…

Amendments to the 2001 CIS Regulations under the Legal Notice 100 of 2009 cited as Capital Ma…

The Fund Managers Association (FMA) was established in 2008, as a Kenyan trade association to promo…

The Capital Markets (Collective Investment Schemes) Regulations, 2001 introduced:▫️Active regulator…

The Capital Markets Authority (CMA) was set up on 15th December 1989 by an Act Parliament, Capital …

In November 1989, the Bill was passed in Parliament and subsequently received Presidential assent.

In November 1988, the Government set up the Capital Markets Development Advisory Council and charge…

The Government further re-affirmed its commitment to the creation of a regulatory body for the capi…

In 1984, a study on the Development of Money and Capital Markets in Kenya was jointly undertaken by…

The Trustee Act amendment 1967 - that commenced on 25th August 1967 guided Unit Trust Trustees inve…

The Unit Trusts Act of 1965 is the original law that established Unit Trusts Schemes in Kenya, used…

Treasury Bonds

The Glosslify™ Spotlight

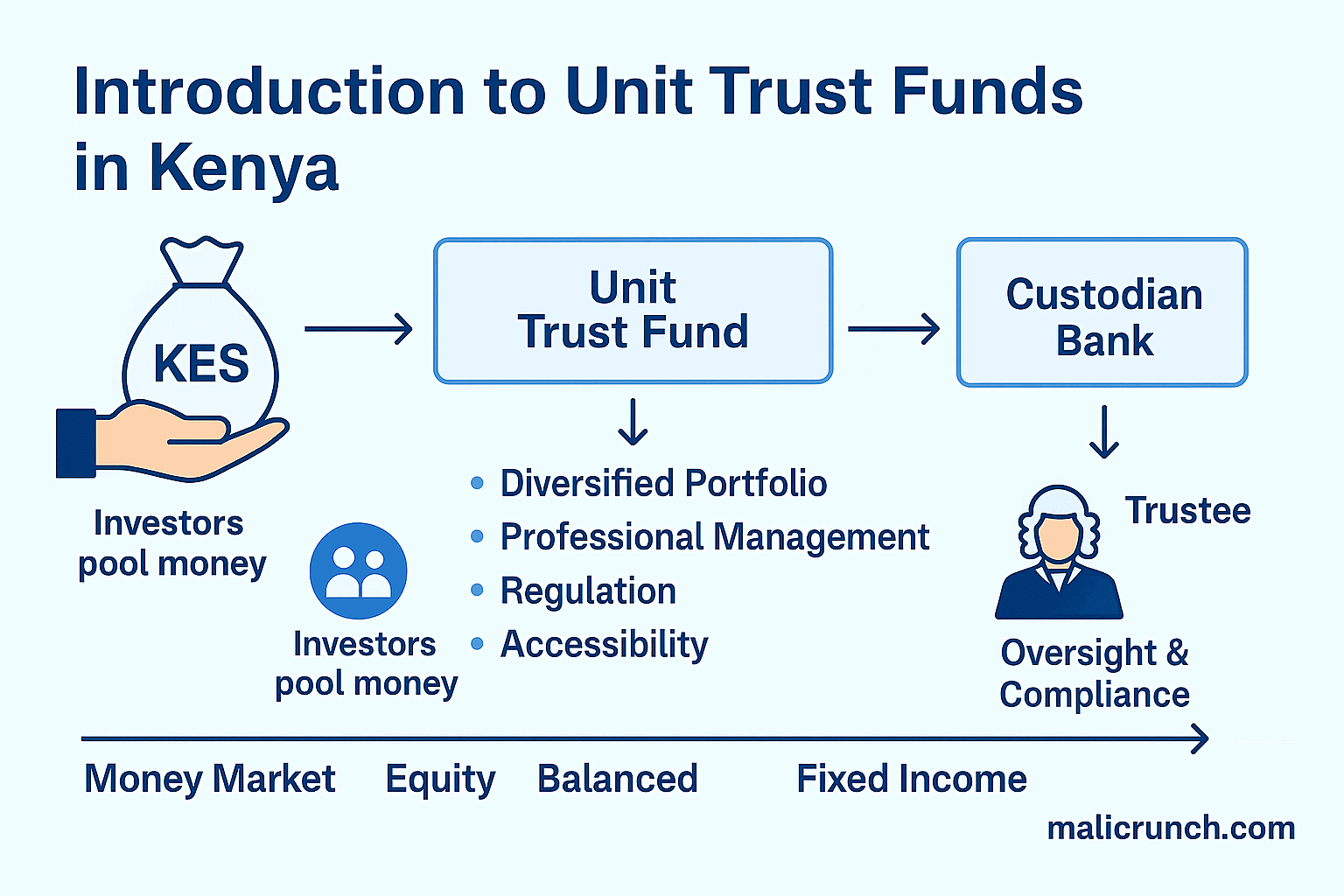

A collective investment scheme in which investors’ contributions are pooled together to purchase a portfolio of financial securities, such as equities (shares), bonds, cash, bank deposits etc. The portfolio is managed by professional fund managers.

Investors contributions/investments into the Pool of funds (unit trust) are used to purchase units. Each unit represents an equal fraction of the total value of the pool of invested money.

When an investor makes an initial investment or makes an additional investment, Units are usually purchased from the fund manager and sold back to the fund manager when a unit holder need to redeem their investments (in this case), units.

The number of units allocated to an investor is calculated by dividing the amount the investor invests by the offer price at the time. As an example, if the offer price for each unit is Kshs 1, an investment of Kshs 10,000 will buy 10,000 units.The value of units moves in accordance with the performance of the unit trust’s assets.

A unit trust has a trust framework.

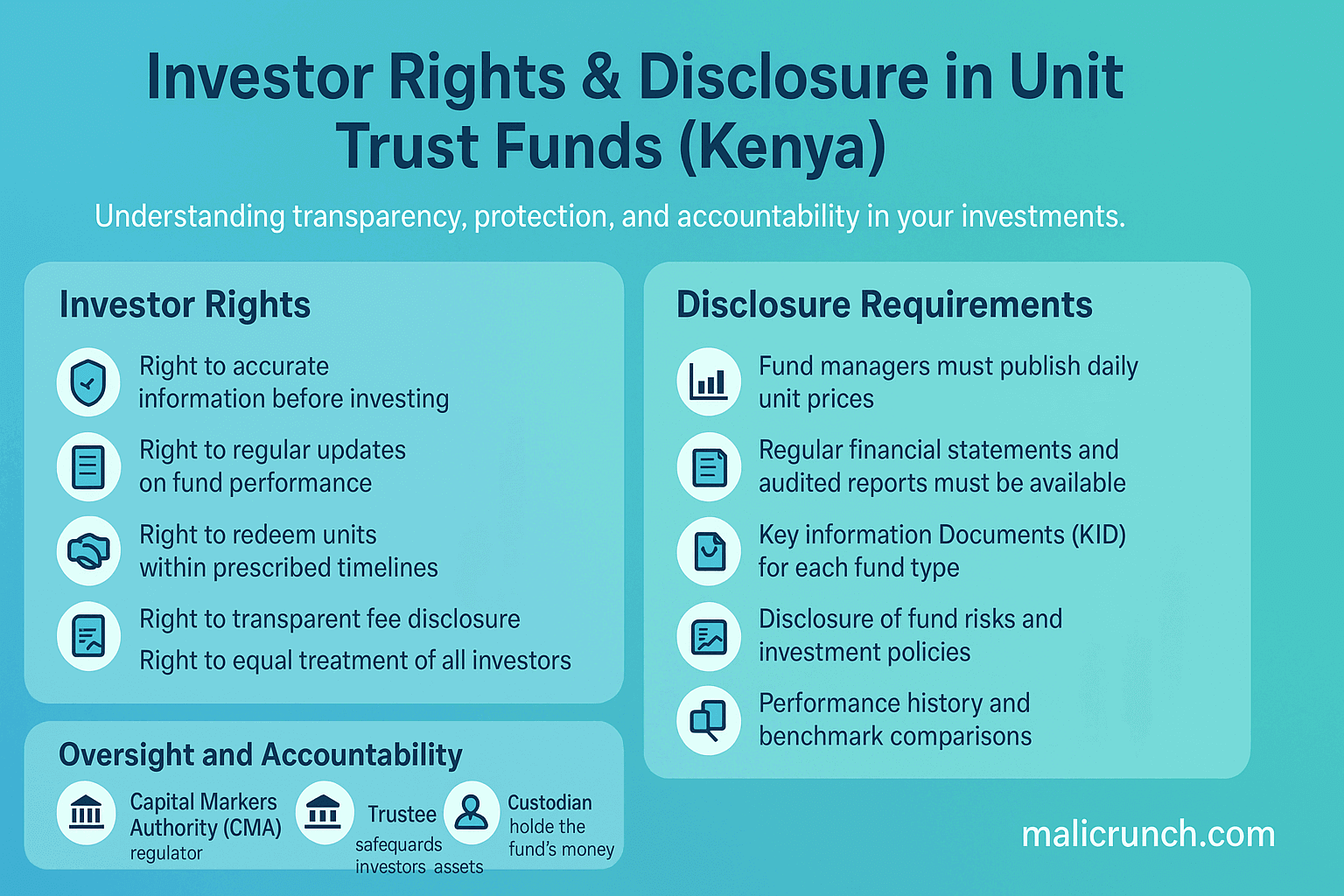

The funds are set up to safeguard investor’s money by separating the various functions among the fund manager, custodian, trustee and auditor.

Unit holders investment and assets purchased are safely held in a custody account overseen by a custodian (usually a CMA approved bank or financial institution).

The Capital Markets Authority (CMA) ensures all the above parties play their roles independently, that investors'funds are safe and that only registered professionals are involved with the affairs of the unit trusts.

The following should be put into consideration:

Your risk profile.

Your preferred time horizon for the investment.

Your financial goals – immediate, short, Medium and Long-term, and

Liquidity- Whether you require regular income or purely looking for capital growth.

Investment returns on a unit trust fund depends on the following:

Returns from the financial markets,

The type of assets within the particular fund portfolio, and

The management skills of the portfolio managers.

The value of equities (shares), bonds and other asset classes that unit trust invests into are determined by financial markets and can rise or fall from time to time. In general, the level of investment return is generally related to the level of risk incurred i.e. the higher the potential risk, the greater the potential return.

You can change any of your static details from;

bank details,

postal address,

signatories,

beneficiaries etc.,

By sending a duly signed instruction to your fund manager so that they can effect the changes. This applies to all clients. In the case of a corporate account, all signatories MUST sign for the same

Credit risk is the risk that a counter party will not meet its obligations under a financial instrunment or client contract, leading to a financial loss. Unit trust schemes can be exposed to credit risk from their operating activities (primary investments), including deposits with financial institutions and other financial instrunments.

Liquidity risk is the risk that the scheme will not be able to meet its financial obligations when they fall due. Schemes are required to manage liquidity to ensure, as far as possible, that they will always have signifiacant liquidity to meet liabilities when due without incurring unacceptable losses or the risk of damaging the their reputation.

Market Risk is the risk that the fair value or future cash flows of a financial instrunment will fluctuate because of changes in market prices.

Unit trust schemes may be exposed to price risk as a result of its holdings in quoted debt instrunments investments, carried at fair value through profit or loss.

Interest Rate risk arises primarily from investments in fixed interest securities that are measured at fair value through profit or loss.

This is a financial risk that exists when a unit trust scheme is affected by a variation in the exchange rate between its local currency and the foreign currencies used in financial transactions.

Operational risk is the risk of loss arising from systems failure, human error, fraud or external events. When controls fail to operate effectively, operational risk can cause damage to reputation, have legal or regulatory implications or lead to financal loss.

In Kenya, Unit Trusts are regulated by Capital Markets Authority. Only unit trust schemes that are approved by the Capital Markets Authority maybe offered for sale to the Kenyan public. Such schemes must comply with the capital markets Act Cap 485A and also the Capital Markets (Collective Investment Schemes) Regulations, 2001.

All Unit trust schemes operators, such as fund managers and trustees, are required to obtain a license from the Capital Markets Authority before commencing operations. The licensing process involves meeting specific criteria, including capital requirements, fit and proper tests for key personnel, and compliance with regulatory guidelines.

All unit trust schemes must clearly define their investment objectives and strategies in their offering documents, such as the prospectus. The Capital Markets Authority regulates the permissible investments, diversification requirements, and restrictions to ensure prudent investment practices and risk management.

Unit trust schemes operators are mandated to provide investors with comprehensive and accurate information regarding the scheme's investment objectives, fees, charges, risks, performance, and financial statements. This ensures transparency and enables investors to make informed decisions. Regular reporting to the Capital Markets Authority is also required.

The fund manager is responsible for actively raising capital, deploying it and managing the investments to meet the fund's investment goals. The fund manager Manages the investment portfolio of the respective schemes.

The trustee Safeguards all interest of unit holders during operations of Unit Trust Scheme, monitors compliance to Trust Deed.Trustees ensure that the fund managers run the trust following the respective fund's investment goals and objectives.

The CMA approved Custodian, who must be affiliated to a commercial bank effectively holds and safeguards all assets and cash of Unit Trust scheme on behalf of the investors and release the money which is invested by the Fund Manager as per the scheme’s policy.

The role of the auditor is to evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent a true and fair view of the financial position, performance, and cash flows of the unit trust scheme.

The role of the Fund administrator is Administration, Distribution and Marketing of the respective fund.

The role of the regulator is to ensure compliance with the capital markets Act Cap 485A and also the Capital Markets (Collective Investment Schemes) Regulations, 2001.

Fund members Provide financial resources to the fund pool for investment.By providing financial resources to the fund pool, fund members enable the unit trust scheme to achieve economies of scale. Pooling resources allows the scheme to access investment opportunities that may not be available or feasible for individual investors.

These are charges incurred by the unit trust fund.

Service fees are paid to the fund manager for the proffessional management of the fund. The fees are charged at a rate inclusive of taxes per annum, computed on the daily fund balances.

Custody fees are paid the fund's custodian for the custodial services to the fund. The fee is charged upto a set percentage maximum of the funds under management, payable monthly and reviewed on an anual basis.

The fund's trustee is paid an annual fee set as a percentage rate of the market value of the fund accrued daily. The fee is paid monthly and is reviewed on an annual basis.

These are charges incurred by the unit trust fund investors.

This is a fee charged on every withdrawal other than the minimum allowed number of withdrawals in a calader month. It is often a fixed amount charged on every subsequent withdrawal to the minimum allowed number of withdrawals.

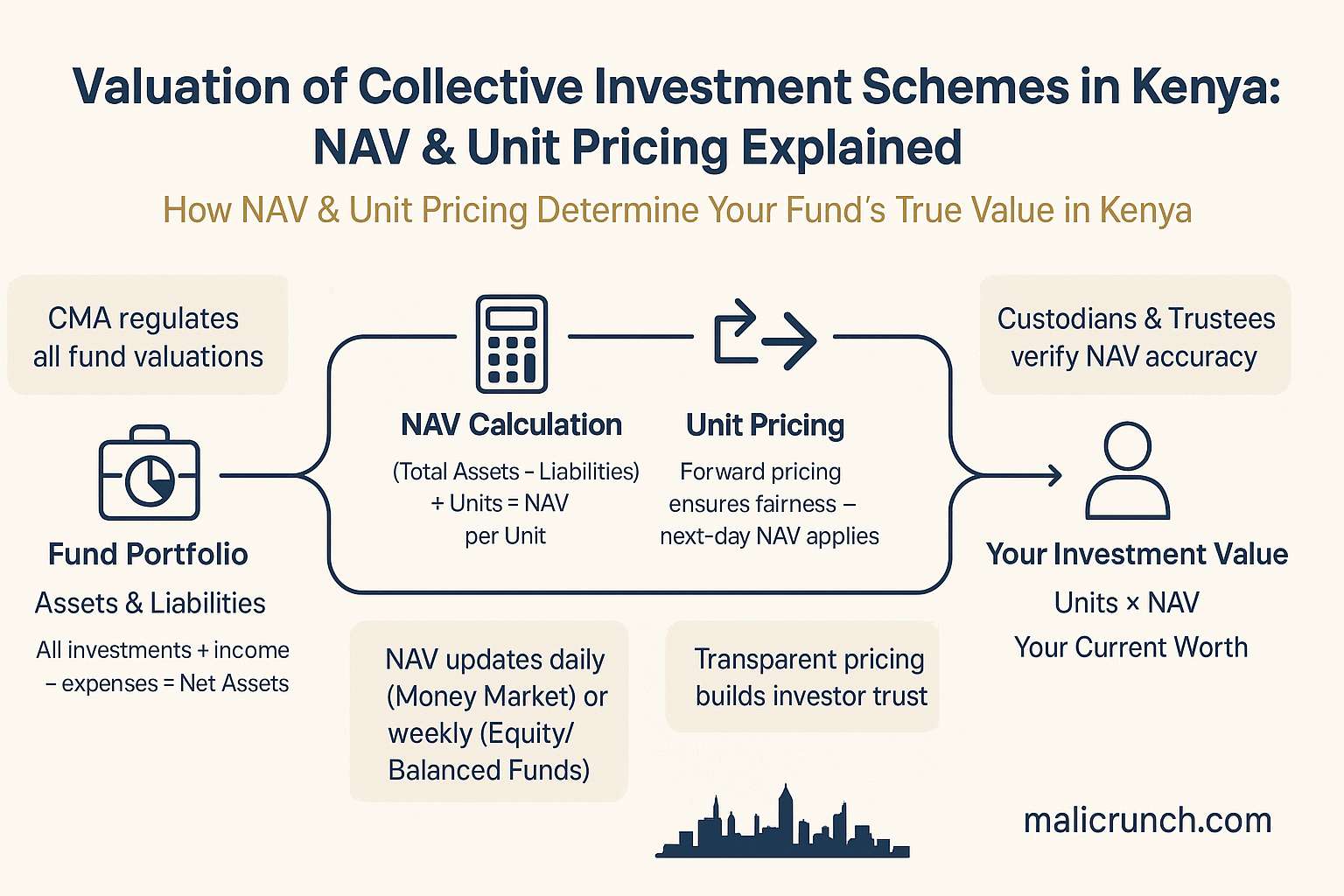

The annual management fee is usually expressed as a percentage of the net asset value (NAV) of the scheme. This fee covers the ongoing costs of managing the scheme, including administrative expenses, research, and portfolio management.

This is a fee charged on every withdrawal other than the minimum allowed number of withdrawals in a calader month. It is often a fixed amount charged on every subsequent withdrawal to the minimum allowed number of withdrawals.